The conversation about digital money in America fundamentally shifted in July 2025. For years, policymakers, technologists, and central bankers debated whether the United States should issue a government-backed digital currency. That debate didn't end with consensus—it ended with a decisive legislative rejection.

While the Anti-CBDC Surveillance State Act sought to bar the Federal Reserve from issuing a retail digital currency directly to the public, the real-world legislative battleground shifted to frameworks designed to bring private stablecoin issuers under federal oversight. Together, these competing efforts represent a significant monetary policy pivot, giving private companies a regulatory green light to digitize the dollar under strict guardrails.

This wasn't an accident. It was the result of an unusual political coalition—privacy advocates worried about government overreach, banking lobbyists protecting their business model, and free-market ideologues who believed Silicon Valley could do it better than Washington. The result? America chose to privatize its digital currency infrastructure rather than build it as a public utility.

Meanwhile, China accelerated in precisely the opposite direction. By September 2025, the digital yuan (e-CNY) had processed over $2 trillion in transactions, integrated into a "dual-center" cross-border architecture designed to challenge dollar dominance. The world's two largest economies made fundamentally incompatible choices about the future of money.

Stablecoins vs. CBDCs: What's the Real Difference?

Despite often being discussed together, stablecoins and central bank digital currencies (CBDCs) are fundamentally different instruments with radically different implications for power and control.

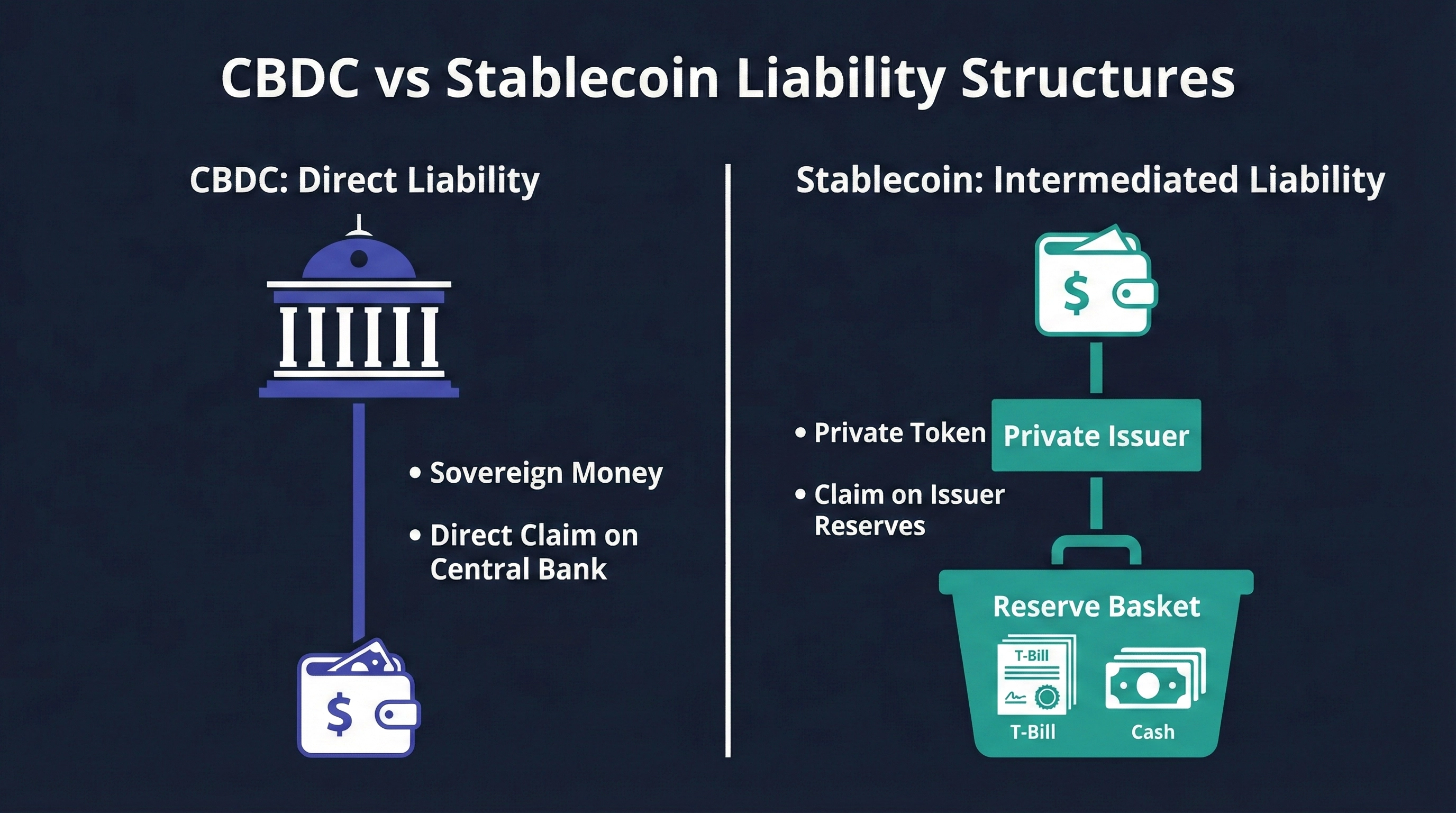

Central Bank Digital Currencies are digital versions of sovereign money issued directly by a nation's central bank. Think of them as the digital equivalent of the physical cash in your wallet, but with a crucial difference: they're a direct liability of the government. When you hold a CBDC, you have a claim directly on the Federal Reserve (or People's Bank of China, or European Central Bank). No intermediary stands between you and the state.

Stablecoins, by contrast, are privately issued digital tokens pegged to a currency like the dollar. When you hold USDC (Circle's stablecoin) or USDT (Tether), you don't have a claim on the U.S. government—you have a claim on a private company that promises to hold enough dollars or dollar-equivalents (like Treasury bills) to redeem your tokens on demand. They're more like digital money market funds than government currency.

The distinction matters profoundly. CBDCs centralize monetary control in the hands of the state, potentially enabling unprecedented surveillance and programmability. Stablecoins distribute issuance across private entities, maintaining the two-tier banking system where private institutions create most of the money supply. One model prioritizes government control and policy flexibility; the other preserves market competition and private innovation.

Why the U.S. Rejected a Retail CBDC

The Anti-CBDC Surveillance State Act (H.R. 1919)

This legislation makes the United States the first major economy to legally prohibit its central bank from issuing retail digital currency. The bill's sponsor, Representative Tom Emmer, framed it as a constitutional firewall against financial surveillance.

The public argument centered on privacy and programmability concerns. Proponents warned that a Federal Reserve digital dollar could technically enable the government to impose granular controls on American spending—restricting purchases of specific goods like firearms or fuel, enforcing expiration dates on stimulus payments, or implementing negative interest rates directly on household savings. China's integration of the digital yuan with its social credit system served as a cautionary tale cited repeatedly in congressional testimony.

But the privacy argument, while genuine for many legislators, masked a more prosaic economic reality: the banking industry viewed a retail CBDC as an existential threat.

Here's why. In the current system, when you deposit money in a bank, you're actually making an unsecured loan to that institution. Your deposit becomes the bank's liability, and the bank uses those funds to make loans and investments. This fractional reserve system is how commercial banks create most of the money supply and generate their profits.

If Americans could instead hold risk-free digital dollars directly with the Federal Reserve—earning the same security as Treasury bonds with the convenience of cash—why would anyone keep significant deposits in a commercial bank? During any financial stress, deposits would instantly flee from banks to the Fed's balance sheet. The very existence of a retail CBDC would make traditional bank deposits structurally inferior, potentially triggering bank runs at digital speed.

The Legislative Battleground: Lummis-Gillibrand & Narrow Banking

The Dual-Banking Compromise

With top-down retail CBDCs viewed as politically toxic, the serious legislative vehicles competing to bring dollar tokens under federal oversight are frameworks like the Lummis-Gillibrand Payment Stablecoin Act and the Clarity for Payment Stablecoins Act.

Rather than forcing a single federal monopoly, these frameworks attempt to preserve America's historic dual-banking architecture through two distinct pathways:

- Federal Trust charters allow non-bank fintechs to apply directly to the Office of the Comptroller of the Currency (OCC), issuing stablecoins subject to direct Federal Reserve balance-sheet supervision.

- State-chartered issuers preserve their right to operate under state banking commissioners up to an aggregate payment ceiling (historically debated around the $10 billion mark), beyond which federal preemption kicks in.

The revolutionary pillar of these drafts is a strict 100% safe-asset reserve mandate. Issuers are legally forced to back tokens exclusively with physical cash, overnight Treasury repo, or short-duration T-bills—effectively outlawing algorithmic backing or commercial paper models.

Stablecoins as a "Synthetic CBDC"

Proposed stablecoin legislation creates what economists increasingly call a "synthetic CBDC"—a privately issued digital dollar that functions like a central bank liability without actually being one.

Consider the economics: When you mint a federally compliant stablecoin, your dollars flow into Treasury bills or Fed-backed bank deposits. When you spend that stablecoin, you're effectively circulating sovereign debt instruments as payment. The issuer becomes a passive custodian, a regulated warehouse for government obligations rather than a credit-creating institution.

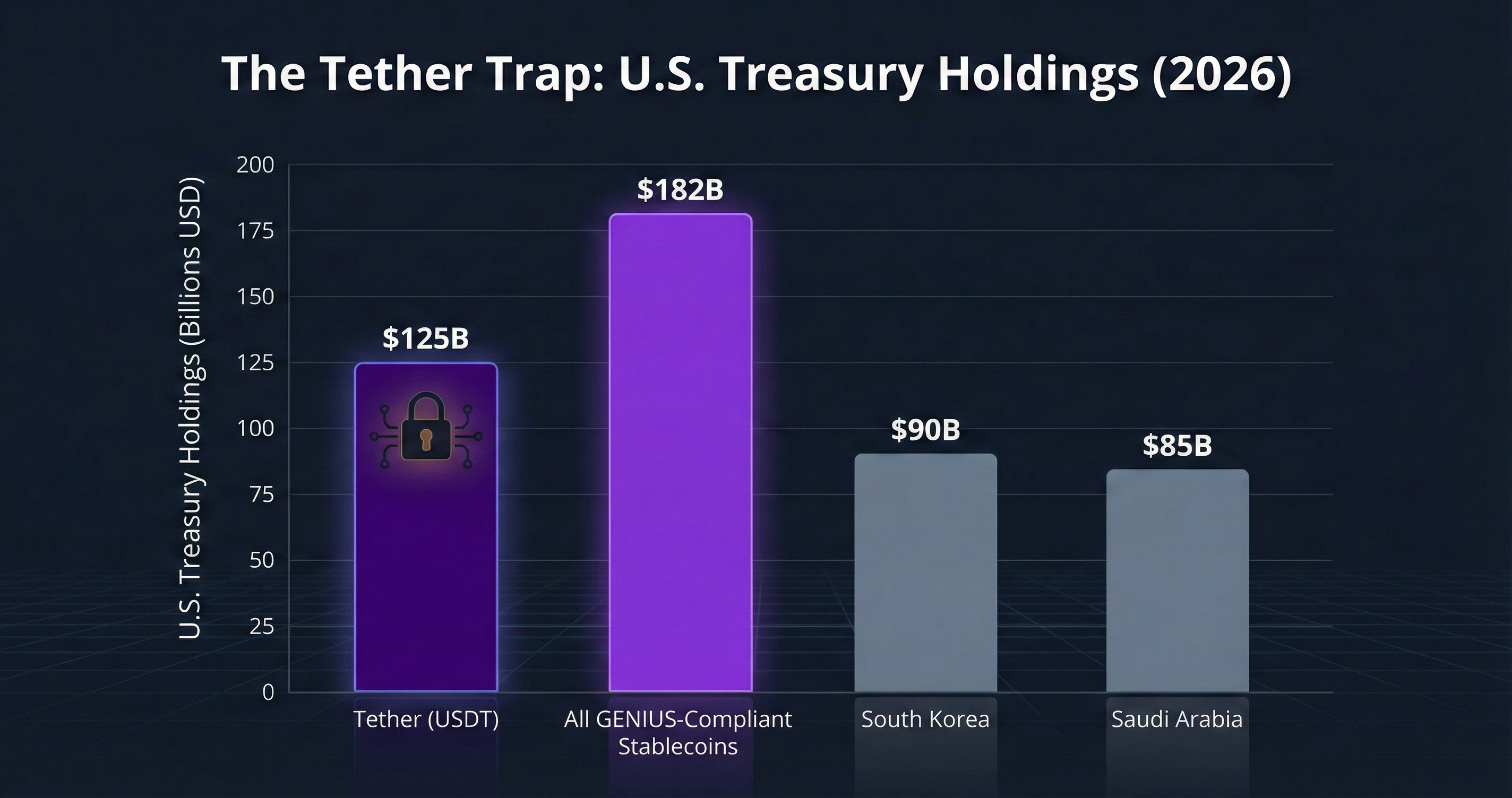

By mid-2025, stablecoin issuers collectively held over $182 billion in U.S. Treasuries—more than the sovereign debt holdings of South Korea or Saudi Arabia. Tether alone held $125 billion. This creates what policy analysts call the "Tether Trap": the U.S. government relies on offshore, sometimes controversial stablecoin issuers as significant buyers of American debt.

Tether's real-world response was highly pragmatic: leveraging its massive Treasury yield to pivot into a borderless institutional financier of AI compute clusters and sovereign commodities.

How This Preserves Bank Power (Deposit Tokens & Narrow Banking)

The traditional banking sector didn't sit passively while stablecoins threatened their deposit base. They launched a technological counter-offensive: tokenized deposits.

The distinction is critical. Stablecoins under these proposed frameworks are narrow banks—they cannot lend and must hold full reserves. Tokenized deposits, issued directly by commercial banks, remain fractional reserve instruments. They're digital representations of traditional bank money, residing on blockchain infrastructure but fully integrated with the capital-efficient lending operations that make banks profitable.

JPMorgan led this charge. In November 2024, it rebranded its blockchain division from Onyx to Kinexys, signaling a shift from experimental technology to core infrastructure. By 2026, Kinexys processes over $2 billion in daily transaction volume, primarily in wholesale repo markets and cross-border settlement.

The industry's most ambitious initiative is the Regulated Liability Network (RLN). A UK pilot running through mid-2026 involves six major banks creating a shared ledger where tokenized deposits from different institutions can settle against each other in real time.

This explains the deeper economics of the proposed frameworks' no-yield provisions. Banks successfully lobbied to ensure that stablecoins cannot compete on returns, only on payment speed and global accessibility. Tokenized deposits can pay interest; regulated stablecoins cannot. This regulatory asymmetry creates a two-tier system: stablecoins for transactions, tokenized deposits for savings and sophisticated treasury management.

The Surveillance Tradeoff No One Talks About

The debate over CBDCs versus stablecoins is often framed as privacy versus surveillance, private innovation versus government control. But the reality is more nuanced and troubling: neither model eliminates surveillance—they just change who's watching.

A Federal Reserve CBDC would centralize transaction visibility with the government. Every payment would potentially flow through a single ledger controlled by the central bank, creating unprecedented capacity for monitoring, taxation enforcement, and economic control.

The American rejection of this model was framed as a victory for privacy and civil liberties. But a regulated private stablecoin system doesn't eliminate surveillance—it privatizes and fragments it. Stablecoin issuers are required to implement "know your customer" (KYC) and anti-money laundering (AML) protocols comparable to traditional banks.

China's CBDC Strategy and the Global Divide

While Washington chose privatization, Beijing doubled down on state control. China's digital yuan (e-CNY) represents the most advanced implementation of the sovereign digital currency model.

By September 2025, the e-CNY had processed 14.2 trillion yuan (approximately $2 trillion) in cumulative transaction volume. The People's Bank of China's response was strategically brilliant: in late 2025, it began paying interest on e-CNY holdings. This represents a fundamental divergence in philosophy. Proposed U.S. stablecoin legislation prohibits interest on stablecoins to protect commercial banks; China mandates interest on digital currency to promote state control.

The more significant development was the international infrastructure. China established a "dual-center" digital currency architecture—an international operations center in Shanghai and a management center in Beijing—specifically designed to facilitate cross-border yuan settlement outside Western financial rails. This connects directly to Project mBridge, the multi-CBDC cross-border payment platform.

mBridge represents the most concrete challenge to dollar dominance. Initially developed as a collaboration between the BIS and central banks from China, Hong Kong, Thailand, and the UAE, the platform successfully demonstrated the ability to settle international transactions in seconds. However, in October 2025, the BIS withdrew from the project after Russian President Vladimir Putin cited mBridge technology as the foundation for a "BRICS Bridge" designed to evade Western sanctions.

Control of mBridge transferred entirely to the participating central banks, effectively transforming it from a neutral technocratic experiment into explicitly geopolitical infrastructure. Parallel to this, the expanded BRICS bloc formalized BRICS Pay, a decentralized financial messaging system designed to replace SWIFT.

What This Means for the Dollar's Global Dominance

The bifurcation of digital currency systems creates paradoxical implications for dollar hegemony. America's decision to privatize its digital dollar through stablecoins simultaneously strengthens and threatens its monetary power.

The strengthening argument: Stablecoins extend dollar reach into markets where traditional banking infrastructure fails or where governments impose capital controls. In Argentina, Nigeria, and Turkey, dollar stablecoins have become the de facto medium for savings and cross-border commerce. This "crypto-dollarization" reinforces American monetary influence even as official reserves decline.

The threatening argument: By fragmenting dollar issuance across dozens of private entities operating on global, permissionless infrastructure, the United States loses direct control over its currency's international circulation. Unlike SWIFT, which the U.S. can effectively choke off, stablecoin infrastructure distributes power across private companies and decentralized networks.

The deeper challenge comes from the East. While dollar stablecoins dominate crypto-native markets, they are irrelevant for the state-to-state settlement that truly determines reserve currency status. China doesn't need its corporations to adopt USDC—it needs Saudi Arabia and Brazil to settle oil and commodities in digital yuan on mBridge rails.

The Future of Digital Money (2026–2030 Outlook)

The monetary landscape of 2026 reveals not convergence toward a unified global financial system, but the hardening of a new digital Iron Curtain. Two incompatible visions of money are now operationally deployed at scale, each optimized for different values and geopolitical objectives.

The Western Stack comprises regulated stablecoins (USDC, PYUSD), tokenized commercial bank deposits (JPMorgan Kinexys, Citi Token Services), and wholesale central bank infrastructure (FedNow, ECB's TARGET2). It prioritizes market efficiency, private innovation, and regulatory clarity while preserving the two-tier banking system.

The Sovereign Stack comprises state-issued CBDCs (e-CNY, digital ruble, eventually digital euro), geopolitical payment rails (mBridge, BRICS Pay, CIPS), and state-controlled messaging infrastructure. It prioritizes policy control, sanctions evasion, and monetary sovereignty.

Neither system has achieved decisive victory. The battle for digital money supremacy will likely play out across several dimensions over the next four years:

- Emerging Market Adoption: Will countries facing U.S. sanctions adopt BRICS Pay infrastructure, or will their citizens continue grassroots dollarization via stablecoins?

- Regulatory Competition: Will Europe's MiCA framework successfully create euro-denominated stablecoins, or will the European market remain captured by regulated U.S. dollar tokens?

- Banking System Stability: Will the growth of narrow-bank stablecoins trigger the credit contraction that Federal Reserve researchers warn about?

- Geopolitical Friction: Will the U.S. Treasury aggressively enforce sanctions on blockchain infrastructure, potentially forcing a "hard fork" between compliant (Western) and non-compliant (Eastern) networks?

The BIS's vision of a unified "Finternet"—a single programmable platform where all financial assets interoperate seamlessly—appears increasingly implausible. Instead, we are heading toward a bifurcated system where Western and Eastern blocs operate fundamentally incompatible monetary infrastructure.

The deepest question isn't technical but philosophical: Is money ultimately a tool of state power or a market phenomenon that emerges from voluntary exchange? The United States, by rejecting the CBDC and embracing regulated private issuance, placed a historic bet that market forces would better preserve dollar dominance than direct state control. China made the opposite bet. The 2020s will reveal which model wins.

FAQ: Stablecoins, CBDCs, and the Digital Dollar

What's the difference between a stablecoin and a CBDC?

A stablecoin is a privately issued digital token pegged to a currency, typically backed by reserves held by the issuing company. A CBDC (Central Bank Digital Currency) is digital money issued directly by a government's central bank. The key difference: with a CBDC, you have a direct claim on the government; with a stablecoin, you have a claim on a private company holding reserves.

Why did the United States ban the Federal Reserve from issuing a retail CBDC?

The official reason was privacy concerns—lawmakers worried that a Fed-issued digital dollar could enable government surveillance of transactions and "programmable money" with spending restrictions. The practical reason was banking industry pressure: if Americans could hold risk-free digital dollars directly with the Fed, commercial bank deposits would become structurally inferior, potentially triggering bank runs.

What is the primary mandate of proposed U.S. stablecoin legislation?

The core objective of frameworks like the Lummis-Gillibrand draft is to enforce a strict 100% reserve requirement backed exclusively by safe, liquid U.S. Treasury bills or cash, effectively turning private stablecoin issuers into regulated narrow banks.

Will regulated stablecoins be allowed to pay interest to users?

No. Major legislative drafts explicitly bar issuers from passing Treasury yield down to token holders. This protects traditional commercial banks by ensuring stablecoins function strictly as payment tools rather than yield-bearing savings accounts.

How is China's approach different?

China is building a state-controlled digital currency (the e-CNY or digital yuan) issued directly by the People's Bank of China. Unlike the U.S. model, China's CBDC does pay interest to holders and is explicitly designed for government oversight and cross-border settlement that bypasses Western financial infrastructure.

About the Author

Founder & Tech ObserverUsman Ghani is the founder of WorthZen and an independent technology observer with a focus on emerging trends, digital tools, and the future of innovation. He shares insights across a wide range of topics including technology, online platforms, and digital ecosystems.